Palantir continues to post standout numbers in 2025. Revenue is on track to grow ~45% year-over-year, with U.S. commercial sales nearly doubling and government contracts expanding more than 50%. Profitability is improving too, with net margins already at 33% and expected to expand steadily.

But valuation tells a different story. At today’s levels, Palantir trades at one of the highest revenue multiples in software. If that premium compresses—as history suggests it will—the company’s financial gains may not translate into major upside for investors.

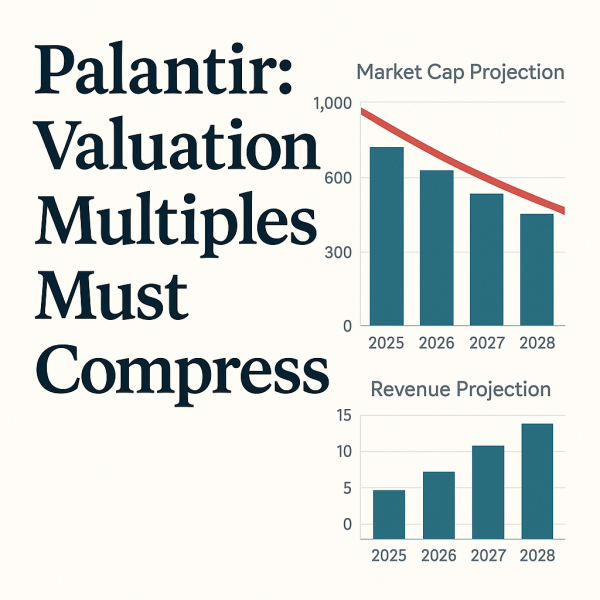

Projection With Multiple Compression

Assumptions:

- Revenue growth: +45% per year (2025–2028)

- P/S multiple: 20% compression per year (from ~74× today)

- Net margin: +1% per year (from 33% in 2025)

| Year | Revenue ($B) | P/S Multiple | Market Cap ($B) | Net Margin | Net Income ($B) |

|---|---|---|---|---|---|

| 2026 | 6.02 | 59.2 | 356 | 34% | 2.05 |

| 2027 | 8.73 | 47.4 | 413 | 35% | 3.05 |

| 2028 | 12.65 | 37.9 | 479 | 36% | 4.55 |

What It Shows

- Revenue soars: more than triples in three years.

- Profitability scales: net income more than doubles, reaching $4.5B by 2028.

- Valuation growth slows: despite explosive fundamentals, market cap rises only modestly—from ~$370B today to ~$479B in 2028.

Why Upside May Be Limited

- Current multiples are historically elevated; even world-class growth cannot fully offset compression.

- Market cap growth (~+29% over three years) lags far behind revenue growth (~+200%).

- In effect, investors may see strong fundamentals but not commensurate share price appreciation.

Conclusion

Palantir is executing exceptionally well—fast growth, rising margins, robust cash generation. But the valuation already prices in much of that success. If multiples continue to normalize, the stock may deliver less upside than the business results suggest.